UPDATE 07/13/2017 – Revised Senate act released this morning. Read it here. I will outline the changes below where pertinent.

The U.S. Senate released their version of a heath care reform act this morning. It is entitled the “Better Care Reconciliation Act of 2017“. It makes important changes to the “American Health Care Act” passed by the U.S. House of Reps back on May 4, 2017. Some of these changes I predicted, some I did not. Like the American Health Care Act, the Better Care Act does not achieve a full repeal of Obamacare but as I have explained, we cannot achieve a full repeal without 60 votes in the U.S. Senate. The Act is a far cry from a free market health care plan but taken in total, it further advances our flag and God willing will restore the individual health insurance marketplace to some semblance of normalcy via less regulations and billions and billions of your taxpayer dollars. Below are the highlights of the Better Care Act of 2017.

Health Insurance Tax Credits will be means tested under this Act

The “American Health Care Act” contained a flat tax credit amount based solely on an applicant’s age. While this is a much simpler way to facilitate tax credits and would involve the I.R.S. as little as possible, it would also require those who are just above the income level necessary to qualify for Medicaid (currently 138% above FPL) to pay significantly more for health insurance than they would have under the P.P.A.C.A. (Obamacare). This is true because Obamacare, like the Better Care Act provides means tested health insurance tax credits. So, the lower your income is the larger your tax credit is. This will ensure that the working poor who are struggling to get off of Medicaid and on to private health insurance will be able to do so for a much more affordable premium than they would have had with the age based tax credits which were the only option included in the American Health Care Act.

Individual and Employer mandates REPEALED

The Better Care Act retains the repeal of both the Individual and the Employer mandates that were included in the American Health Care Act. So, the federal government will no longer be able to force you to purchase insurance using the threat of an I.R.S. penalty.

Obamacare taxes REPEALED and Cadillac Tax “delayed” until 2026

Let’s just be honest. The Cadillac Tax is never going to happen. The employer sponsored health insurance lobbying groups are just too powerful. Can we finally just admit this? That stated, repealing other Obamacare taxes is a great start. Here’s what goes bye-bye:

Tax on health insurance – NO LONGER REPEALED as of 7/13/2017

Tax on employee health insurance premiums REPEALED

Tax on health insurance plan benefits REPEALED

Tax on prescription medications REPEALED

Tax on OTC – Over The Counter – medications REPEALED

Tax on Medical Devices REPEALED

Tax on Chronic Care REPEALED

Tax increase on Medicare – NO LONGER REPEALED as of 7/13/2017

Tax on tanning REPEALED

Tax on net investment – NO LONGER REPEALED as of 7/13/2017

Tax on Health Savings Accounts REPEALED

Tax on Flexible Spending Accounts (where contributions are limited) REPEALED

Tax BREAK for health insurance company executives REMOVED as of 7/13/2017

Preexisting conditions COVERED but WHERE is the 30% penalty for system gamers?

The American Health Care Act allowed health insurers to apply a 30% underwriting load to those who attempt to wait until they are sick to buy health insurance. This was designed to prevent system gaming which increases the cost for everyone. Whilst the Better Care Act is clear on the fact that preexisting conditions are covered, it is not clear on whether or not insurers will be allowed to apply an underwriting load to system gamers. If this load or something like it is not added to the final legislation during conference you can kiss the entire individual health insurance market goodbye because there will be no reason for anyone to maintain health insurance on a consistent basis. Instead they will jump on an off plans when they “need” them and you can sayonara to the few remaining health insurers left in America. Hello Senators! Hello! McFly??!!!

June 26, 2017 UPDATE: Kudos to Senate Republicans for echoing 1996 HIPAA law and longer standing Department of Labor COBRA rules by adding a 6 month waiting period for coverage of preexisting conditions for those who have a lapse in coverage of more than 63 days. This should significantly curb adverse selection by ensuring that Americans keep consistent health insurance coverage. Some sort of penalty for system gamers who wait until they are sick to buy health insurance had to be included.

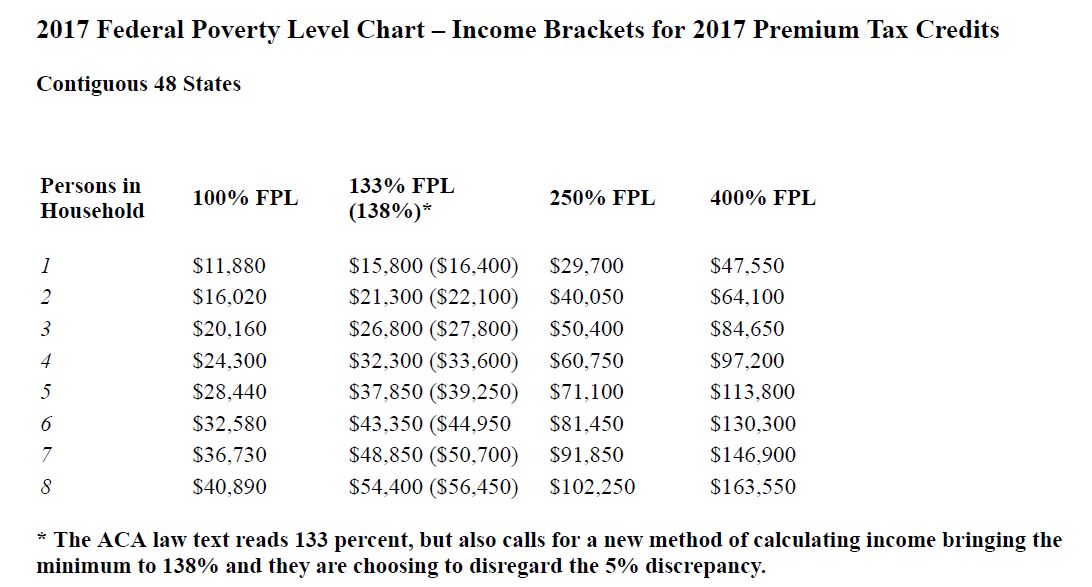

Advance Premium Tax Credit eligibility threshold reduced to 350% above FPL

Under Obamacare, an individual with MAGI – Modified Adjusted Gross Income – higher than 400% of FPL – Federal Poverty Level – ($47,520 annually) would not qualify for an APTC – Advance Premium Tax Credit. Under the Better Care Act, that eligibility threshold is reduced to 350% of FPL or $42,300 annually. Below are charts on how APTC eligibility cut-offs will change based on your family size:

APTC eligibility cut-off under Obamacare

$47,520 for an individual

$64,080 for a couple or family of two

$80,640 for a family of three

$97,200 for a family of four

$113,760 for a family of five

$130,320 for a family of six

APTC eligibility cut-off under Better Care Act

$42,300 for an individual

$57,000 for a couple or family of two

$71,500 for a family of three

$86,300 for a family of four

$101,000 for a family of five

$115,600 for a family of six

You can also use this convenient Federal Poverty Level calculator here.

Advance Premium Tax Credits will now be available to those UNDER poverty line

The Better Care Act will dramatically improve options for more than 2 million Americans who are stuck in a difficult situation in the 19 states that did not expand Medicaid under Obamacare. These people have incomes that are too small to be eligible for Advance Premium Tax Credits used to buy private health insurance while also having income too high to qualify for Medicaid (incomes between 100% and 138% of Federal Poverty Level). So, they’re stuck between a rock and a hard place. The Better Care Act ensures they will now qualify for Advance Premium Tax Credits to purchase private health insurance. This should lead to a significant improvement in health outcomes for these people.

Cost Sharing Reduction subsidies to continue all the way to 2020

Cost Sharing Reduction subsidies are an additional health insurance subsidy available to those with a MAGI lower than 250% of FPL. These subsidies lower deductibles, co pays, coinsurance and other out-of-pocket expenses the policy holder otherwise would incur. Continuation of these subsidies until 2020 may be the biggest bone of contention between the House and the Senate when the Better Care Act gets to the conference committee. This is because House Republicans sued to stop billions in Cost Sharing Reduction subsidies in 2014 since the money was never appropriated by congress, making those expenditures unconstitutional. A federal district court judge ruled in favor of House Republicans and thus far even though he has the power to stop them, President Trump has continued these subsidies tentatively. The Better Care Act ensures they will continue until the year 2020. The continuation of CSR’s will most likely induce some of the 83 health insurers who have left the individual market to return since the CBO estimates that H.H.S. will pay $7 billion in subsidies to health insurers and that total could rise to $16 billion by 2027 which is why the Better Care Act ends Cost Sharing Reduction subsidies permanently in 2020. That end date could result in a compromise.

Benchmark health plan changed from a “Silver” plan to a “Bronze” plan.

This action alone should be responsible for 15% or more in premium reductions across the board. Heretofore, states have being required to use a more expensive “Silver” plan as their benchmark plan resulting in higher premiums for millions of Americans.

CATASTROPHIC PLANS NOW AVAILABLE TO ANYONE AT ANY AGE as of 7/13/2017

The PPACA (Obamacare) only allows those under the age of 30 to buy Catastrophic plans

States can opt out of EHBs but not Community Rating or Preexisting Conditions

The American Health Care Act allowed states to file for a waiver from the requirement to include EHBs – Essential Health Benefits – as defined by Obamacare and it also allowed them to file a waiver from the Community Rating requirement. The Better Care Act also allows states to file a waiver from EHBs but it does not allow them to file a waiver from the Community Rating requirement. While Community Rating does allow health insurers to vary the premium rate charged for an individual or small group plan based on family size, geography, age and tobacco use. It does not allow health insurers to vary premium rates based on an applicant’s expected health status or claims experience. So, preexisting conditions will continue to be covered in all states regardless of any waivers.

UPDATE 7/23/2017 – Revised Senate act includes revised “Cruz-like” amendment

Even though Senator Cruz’s original amendment did not make it into the revised Senate Act. An amendment that borrows much from his original amendment did. This amendment creates a new fund for those with high medical costs. A health insurer can tap into this new fund by offering at least one Obamacare compliant plan. That insurer can then offer other non-Obamacare compliant plans that do not include the following:

1.) The guaranteed issue requirement waived. These plans can medically underwrite, meaning that an applicant can be denied coverage for one of these plans.

2.) The Community rating requirement waived. These plans can charge one more based on an applicant’s health history or a preexisting condition.

3.) The Essential Health Benefit requirement. These plans do not have to include the PPACA mandated “Essential Health Benefits“.

PLEASE NOTE: Even though these non compliant plans can be sold via this new “Cruz-like” amendment, the revised Senate act still requires ALL states to have a High Risk Pool or other risk abatement program in place for those in the individual health insurance marketplace that are denied coverage for a non-Obamacare compliant plan based on their health history or a preexisting condition. Also, BOTH types of health plans (Obamacare compliant and non-Obamacare compliant) will be included in the same pool of risk. That last distinction there may end up defeating the entire purpose of this new “Cruz-like” amendment since those with lower cost non-Obamacare compliant plans will still end up subsidizing those with Obamacare compliant plans (via higher health insurance premiums) since all will be in the same pool of risk.

Hyde amendment wording is followed when restricting funding for abortion

Health insurance purchased using funding from the Better Care Act cannot cover abortions unless they are performed to save the life of the mother or for victims of rape and incest as originally outlined in the Hyde amendment. Medical providers are also prohibited from using any funds allocated under this Act for abortions that are not specifically referred to in the Hyde amendment.

Medical Loss Ratios to be determined by the states NOT the Federal government.

Beginning in 2019 the Better Care Act will allow states to design their own MLR calculations. This action may also spur smaller health insurers to return to the individual market since (depending on the state) they may no longer be restricted to a 15% or 20% operating margin. This will also allow states to determine if Broker/Agent commissions should be included in MLR calculations. Just imagine if we had more licensed and experienced broker/agents and less inexperienced, unlicensed Obamacare “Navigators”. Excluding broker/agent commissions from the MLR calculation will once again entice broker/agents to return to the individual marketplace (there are very few of us left who cater to the individual marketplace). This action would save consumers hours and hours of frustrating time on the phone at Healthcare.gov. Time that is far too often spent without resolving issues and sometimes even exacerbating them.

Age based Community Rating restored to a 5 to 1 ratio

The American Health Care Act restored Age Based Community Rating from 3 to 1 as it was mandated under Obamacare to 5 to 1 which should entice the all important young invincibles to reenter the individual health insurance market place. The Better Care Act keeps this 5 to 1 ratio in place. Obamacare placed a heavy burden on younger people by requiring them to pay much more for health insurance in order to subsidize older people. With the Better Care Act, young people should see a significant drop in premiums because the amount they pay for health insurance will no longer be dramatically increased in order to provide a small reduction in premium for Americans in their 50s and 60s. Increasing premiums for young people does nothing but drive them out of the individual marketplace and when they leave, premiums increase for everyone which is exactly what we witnessed under Obamacare.

ERISA amended so states can cooperate with Fed on Small Business Health Plans

The language is a bit vague here but if this Act allows independent contractors or even members of certain trade associations to band together and share risk I am all for it. I do believe that is the intent behind the ERISA amendment in the Better Care Act.

Medicaid Expansion gone by 2023. States have Block Grants or Per Capita options.

Medicaid is unsustainable by all assessments. So, something has to be done to improve it. Throughout the Better Care Act, states are allowed the option to pursue new ways of improving care and controlling costs via flexible design and quality improvement metrics. If states meet those metrics there is an $8 billion fund they can tap into. In addition, the states have the option to design work requirements, none of which can apply to pregnant women, the blind, those attending school or the disabled. But those who can help themselves, should at least try to help themselves so that more money is left for those who are truly in need. The Better Care Act phases out Obamacare Medicaid expansion over the next four years with 90% of current federal funding for the year 2020 and then a reduction in that federal funding by 5% a year until 2023 when Obamacare Medicaid expansion will end for good. Also, single individuals without dependent children will not be allowed to join Medicaid under Obamacare Medicaid expansion after the year 2020. Advance Premium Tax Credits for private health insurance will however be available to those who lose eligibility for Obamacare Medicaid expansion as the program is slowly eliminated. In addition by 2025 Medicaid will be capped at the rate of growth for all goods, not just the inflation rate in medical prices. So, there is a strong impetus for states to start reforming their Medicaid programs now, not later.

UPDATE 7/13/2017 – Disproportionate Share Hospital payments now allowed to fund hospitals for uncompensated care. Calculation methodology is changed from per Medicaid enrollee to per insured.

HSA deposit amounts will now match your total health plan out-of-pocket risk.

This is a no brainer which is why it was also included in the American Health Care Act. In addition, a 60 day grace period will be allotted for those who purchase an HSA – Health Savings Account – qualified HDHP – High Deductible Health Plan – and incur claims before they have a change to set up their HSA. Those claims incurred before the HSA is set up (and after the HDHP is effective) will also be counted as Qualified Medical Expenses under IRS section 502. In addition, both spouses can now make additional make up contributions providing of course that they are both over the age of 55.

UPDATE: 6/30/2017 Senate adds the ability to use your HSA contributions (for the first time ever) to pay for health insurance premiums. Historically, those funds could only be used to pay for Long Term Care health insurance premiums. This is a GREAT addition!

AND NOW FOR THE SPENDING

$62 billion appropriated for Long-Term state stability & innovation through 2026

The following appropriations are made in the Better Care Act to establish or maintain a program or mechanism to provide financial assistance to help high-risk individuals, including by reducing premium costs for such individuals, who have or are projected

to have a high rate of utilization of health services, as measured by cost, and who do not have access to health insurance coverage offered through an employer, enroll

in health insurance coverage under a plan offered in the individual market.

This money can also be used to establish or maintain a program to enter into arrangements with health insurers to help stabilize premiums and promote state health insurance market participation and choice in plans offered in the individual health insurance market place.

It can also be used to provide payments for health care providers for the provision of health care services, as specified by the administrator. To provide assistance to reduce out-of-pocket costs, such as copayments, coinsurance, and deductibles, of individuals enrolled in plans offered in the individual market place.

$8 billion for year 2019

$14 billion for year 2020

$14 billion for year 2021

$6 billion for year 2022

$6 billion for year 2023

$5 billion for year 2024

$5 billion for year 2025

$4 billion for year 2026

$70 billion MORE added to State stability fund under revised act as of 7/13/17.

$50 billion Short-Term assistance to repair coverage access disruption through 2021

The following appropriations are made to fund arrangements with health insurers to address coverage and access disruption and respond to urgent health care needs

within States:

$15 billion for year 2018

$15 billion for year 2019

$10 billion for year 2020

$10 billion for year 2021

$15 billion individual market stabilization fund for years 2019 through 2021

$5 billion per year is appropriated in order to stabilize premiums and incentivize health insurers to return to the individual marketplace during years 2019, 2020 and 2021.

Additional appropriations also included in the Better Care Act

Additional $422 million appropriated in 2017 for Community Health Centers

$2 billion to combat the opioid crisis. UPDATE: Increased to $45 billion on 6/30/2017

$8 billion for states achieving quality performance metrics in improving Medicaid/CHIP

$500,000,000 appropriated to implement the Better Care Act.

You can read the entire Better Health Care Reconciliation Act of 2017 by clicking below:

https://www.budget.senate.gov/imo/media/doc/SENATEHEALTHCARE.pdf

{kind=link}